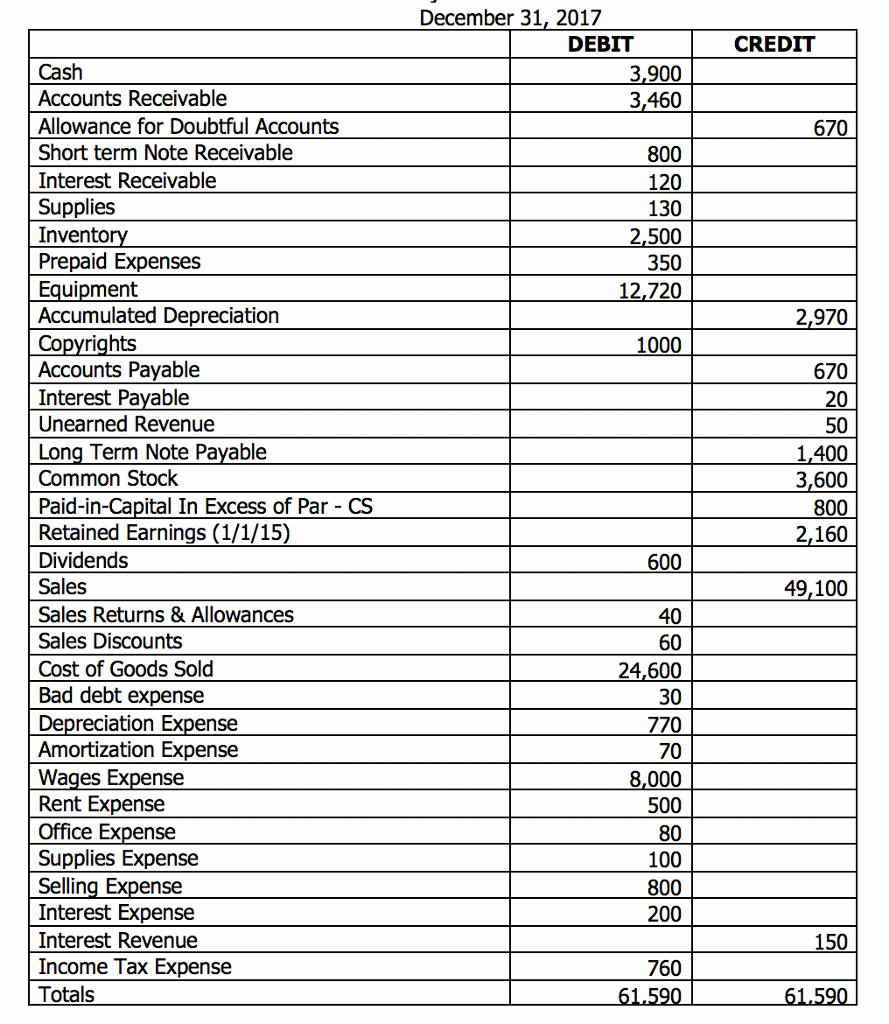

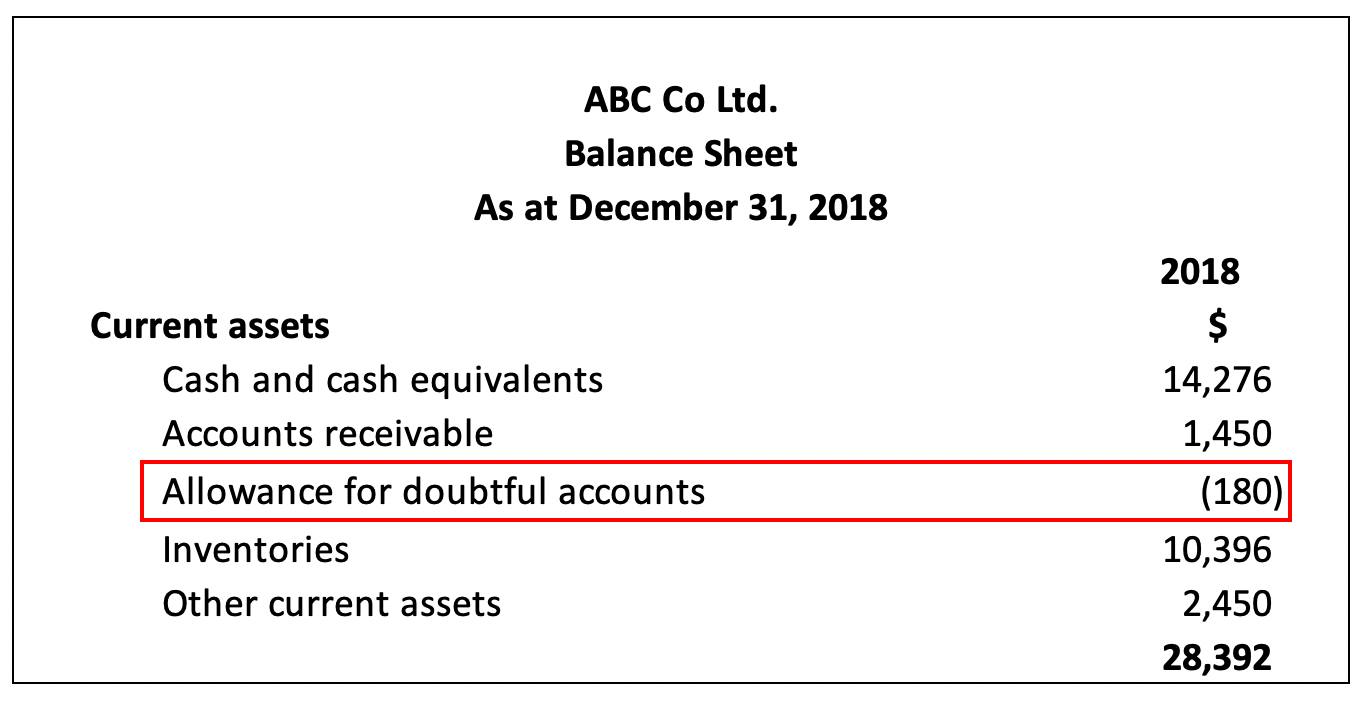

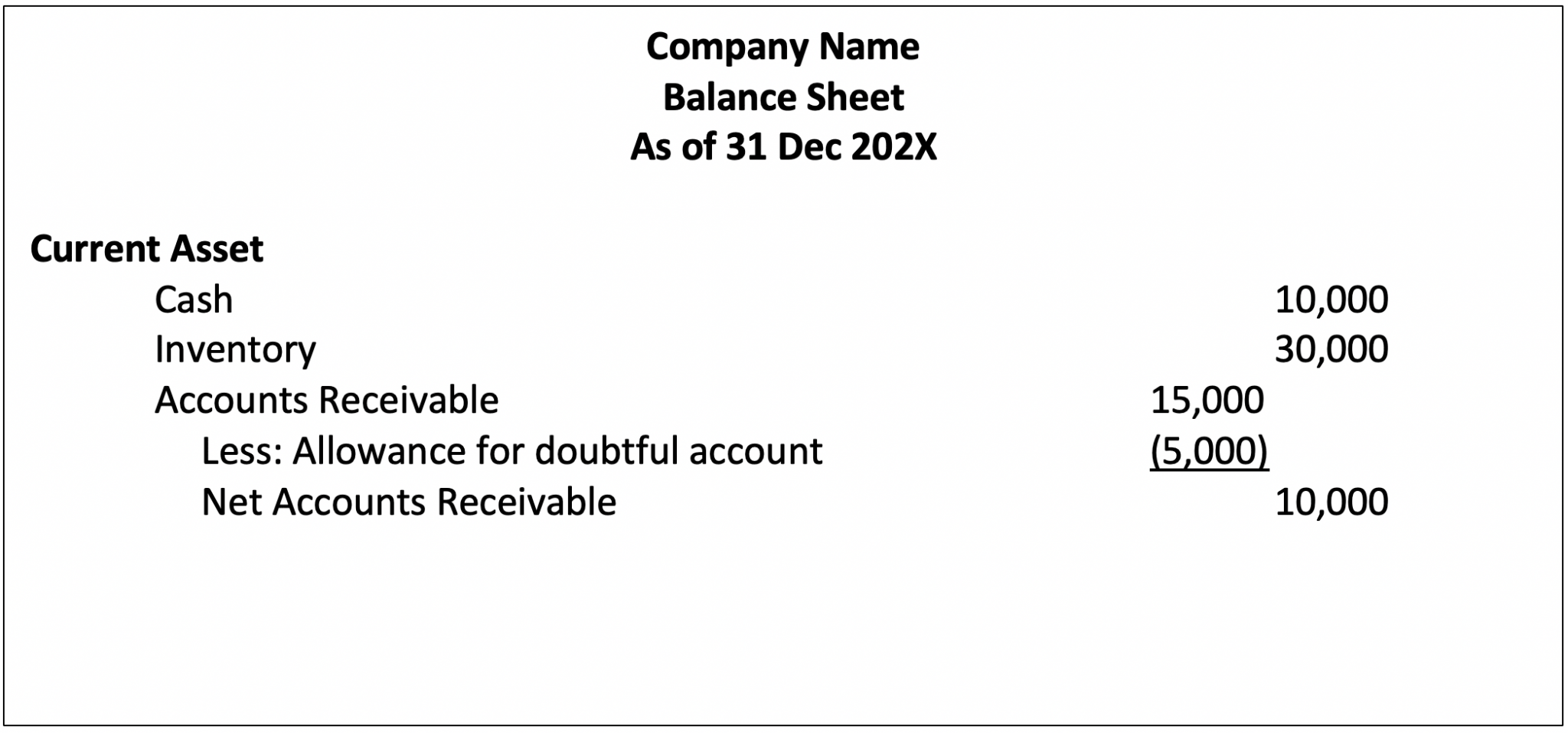

Allowance For Doubtful Accounts On Balance Sheet - The purpose of the allowance for doubtful accounts is to estimate how many customers out of the 100 will not pay. The doubtful account in balance, which records. Units should consider using an allowance for doubtful accounts when they are regularly providing goods or services “on credit” and have experience with the collectability of those. Accounts receivable present in the balance sheet is the net amount, which remains after deducting the allowance for the doubtful account. This deduction is classified as a. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company’s balance sheet. What is an allowance for doubtful accounts? The $1,000,000 will be reported on the balance sheet as accounts receivable. The allowance for doubtful accounts is a company's educated guess about how much customers owe that will never come in.

Accounts receivable present in the balance sheet is the net amount, which remains after deducting the allowance for the doubtful account. The $1,000,000 will be reported on the balance sheet as accounts receivable. The doubtful account in balance, which records. The purpose of the allowance for doubtful accounts is to estimate how many customers out of the 100 will not pay. What is an allowance for doubtful accounts? This deduction is classified as a. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company’s balance sheet. The allowance for doubtful accounts is a company's educated guess about how much customers owe that will never come in. Units should consider using an allowance for doubtful accounts when they are regularly providing goods or services “on credit” and have experience with the collectability of those.

The doubtful account in balance, which records. The allowance for doubtful accounts is a company's educated guess about how much customers owe that will never come in. What is an allowance for doubtful accounts? The purpose of the allowance for doubtful accounts is to estimate how many customers out of the 100 will not pay. Accounts receivable present in the balance sheet is the net amount, which remains after deducting the allowance for the doubtful account. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company’s balance sheet. This deduction is classified as a. The $1,000,000 will be reported on the balance sheet as accounts receivable. Units should consider using an allowance for doubtful accounts when they are regularly providing goods or services “on credit” and have experience with the collectability of those.

Classified Balance Sheet Allowance For Doubtful Accounts

The doubtful account in balance, which records. The allowance for doubtful accounts is a company's educated guess about how much customers owe that will never come in. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company’s balance sheet. The $1,000,000 will be reported on the balance sheet as accounts receivable..

Accounts Receivable Journal Entry Example Accountinguide

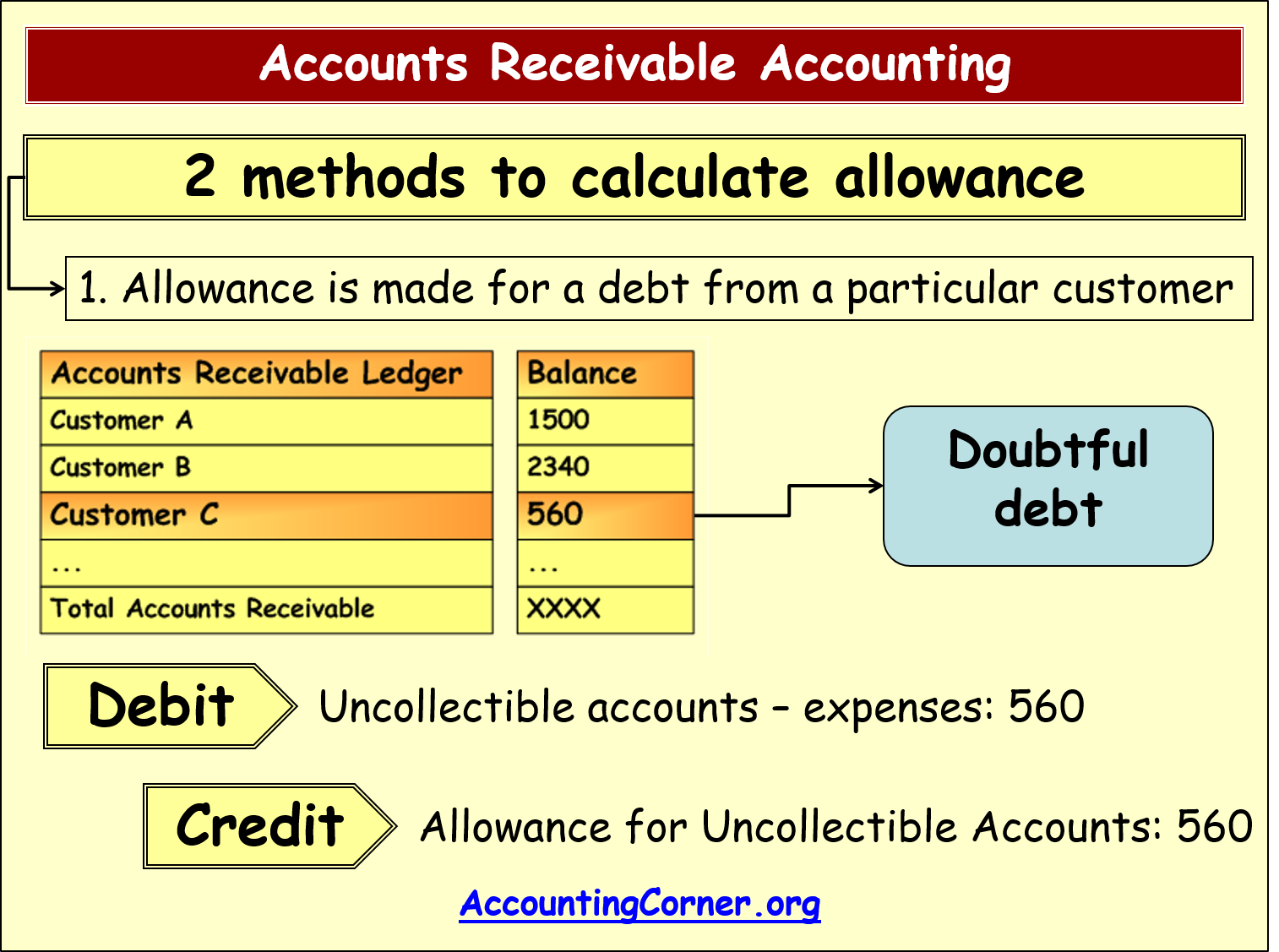

The doubtful account in balance, which records. What is an allowance for doubtful accounts? This deduction is classified as a. Units should consider using an allowance for doubtful accounts when they are regularly providing goods or services “on credit” and have experience with the collectability of those. The allowance for doubtful accounts is a reduction of the total amount of.

How to Account for Doubtful Debts 11 Steps (with Pictures)

Units should consider using an allowance for doubtful accounts when they are regularly providing goods or services “on credit” and have experience with the collectability of those. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company’s balance sheet. The $1,000,000 will be reported on the balance sheet as accounts receivable..

Accounting Unit 5 Part 3 Allowance for Doubtful Accounts

Accounts receivable present in the balance sheet is the net amount, which remains after deducting the allowance for the doubtful account. The $1,000,000 will be reported on the balance sheet as accounts receivable. The doubtful account in balance, which records. Units should consider using an allowance for doubtful accounts when they are regularly providing goods or services “on credit” and.

allowancefordoubtfulaccounts8

Accounts receivable present in the balance sheet is the net amount, which remains after deducting the allowance for the doubtful account. The $1,000,000 will be reported on the balance sheet as accounts receivable. This deduction is classified as a. Units should consider using an allowance for doubtful accounts when they are regularly providing goods or services “on credit” and have.

Bad Debt Expense and Allowance for Doubtful Account Accountinguide

The $1,000,000 will be reported on the balance sheet as accounts receivable. What is an allowance for doubtful accounts? The purpose of the allowance for doubtful accounts is to estimate how many customers out of the 100 will not pay. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company’s balance.

Allowance for Doubtful Accounts Balance Sheet Example YouTube

The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company’s balance sheet. What is an allowance for doubtful accounts? This deduction is classified as a. The purpose of the allowance for doubtful accounts is to estimate how many customers out of the 100 will not pay. Accounts receivable present in the.

Allowance for Doubtful Accounts Personal Accounting

The $1,000,000 will be reported on the balance sheet as accounts receivable. The allowance for doubtful accounts is a company's educated guess about how much customers owe that will never come in. This deduction is classified as a. Units should consider using an allowance for doubtful accounts when they are regularly providing goods or services “on credit” and have experience.

Allowance for Doubtful Debt Double Entry

The purpose of the allowance for doubtful accounts is to estimate how many customers out of the 100 will not pay. What is an allowance for doubtful accounts? The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company’s balance sheet. This deduction is classified as a. The allowance for doubtful accounts.

Allowance for Doubtful Accounts Definition and Examples Bookstime

The allowance for doubtful accounts is a company's educated guess about how much customers owe that will never come in. What is an allowance for doubtful accounts? The doubtful account in balance, which records. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company’s balance sheet. The $1,000,000 will be reported.

What Is An Allowance For Doubtful Accounts?

The purpose of the allowance for doubtful accounts is to estimate how many customers out of the 100 will not pay. The doubtful account in balance, which records. The $1,000,000 will be reported on the balance sheet as accounts receivable. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company’s balance sheet.

The Allowance For Doubtful Accounts Is A Company's Educated Guess About How Much Customers Owe That Will Never Come In.

Accounts receivable present in the balance sheet is the net amount, which remains after deducting the allowance for the doubtful account. This deduction is classified as a. Units should consider using an allowance for doubtful accounts when they are regularly providing goods or services “on credit” and have experience with the collectability of those.